What will the Real Estate Recovery Look Like?

Real estate performance is cyclical; sustained market declines are often followed by strong market appreciation, but the shape of each cycle and the period of recovery often differ depending on the cause of the initial shock to the market.

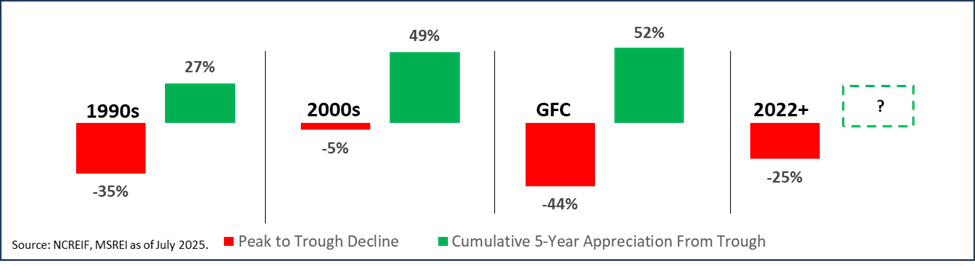

Private Real Estate Prior Cycle Value Declines and Appreciation (Levered %)

In the 1990s, an overhang of excess supply and risky CRE lending depressed pricing and transaction activity for several years. Recovery required banks to repair balance sheets, time for excess supply to clear, and cap rates (percentage yield generated by a property calculated by dividing net operating income by the property value) to compress over multiple years. The early 2000s decline was less of a systemic shock and more driven by the dot-com crash. Markets and sectors with higher tech concentration saw sharper declines, but the overall trough was relatively shallow.

The 2007-09 Global Financial Crisis (GFC) was characterized by deep losses, driven by a massive, systemic credit shock tied to U.S. housing and structured finance. Recovery was a multiyear process, aided by lower interest rates and solid demand and income growth in select sectors, particularly industrial and residential.

Over the past year, several indicators have shown signs of recovery in the commercial real estate market; however, the strength of the recovery remains to be determined. Transaction volumes have increased, price declines have moderated, and financing activity has picked up across sectors (though financing for the office sector remains challenged). Lower interest rates, minimal new supply, and a relatively healthy economic backdrop should be supportive of rent growth and a moderate recovery in valuations going forward. However, economic factors, including the health of the labor market, inflation, and the path of interest rates will play a significant role in determining the shape of the recovery.

There is no single answer on how long a recovery will take and the amount of appreciation that follows a market decline. Supply/demand dynamics in specific sectors and markets will vary, and some sectors and markets will recover faster than others – meaning asset, market, and submarket selection will be critically important in separating the winners and losers during this next phase of the real estate cycle.

This information is intended for institutional use only. Performance and allocations are for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities or investment products. It is intended for the exclusive use of the person(s) to whom it was provided.